{kind=link}

Blockchain technology, once primarily associated with the volatile world of cryptocurrency, is rapidly carving out a new identity across African nations.

As noted in the Africa Blockchain Report 2024, a collaboration between Absa Corporate and Investment Banking (CIB) and Crypto Valley Venture Capital (CV VC), a notable shift is underway.

The technology is moving from an ordinary asset to a foundational tool for solving some of Africa’s most persistent financial challenges in the banking and agricultural sectors.

This development attracts investment and positions Africa as a leader for blockchain innovation.

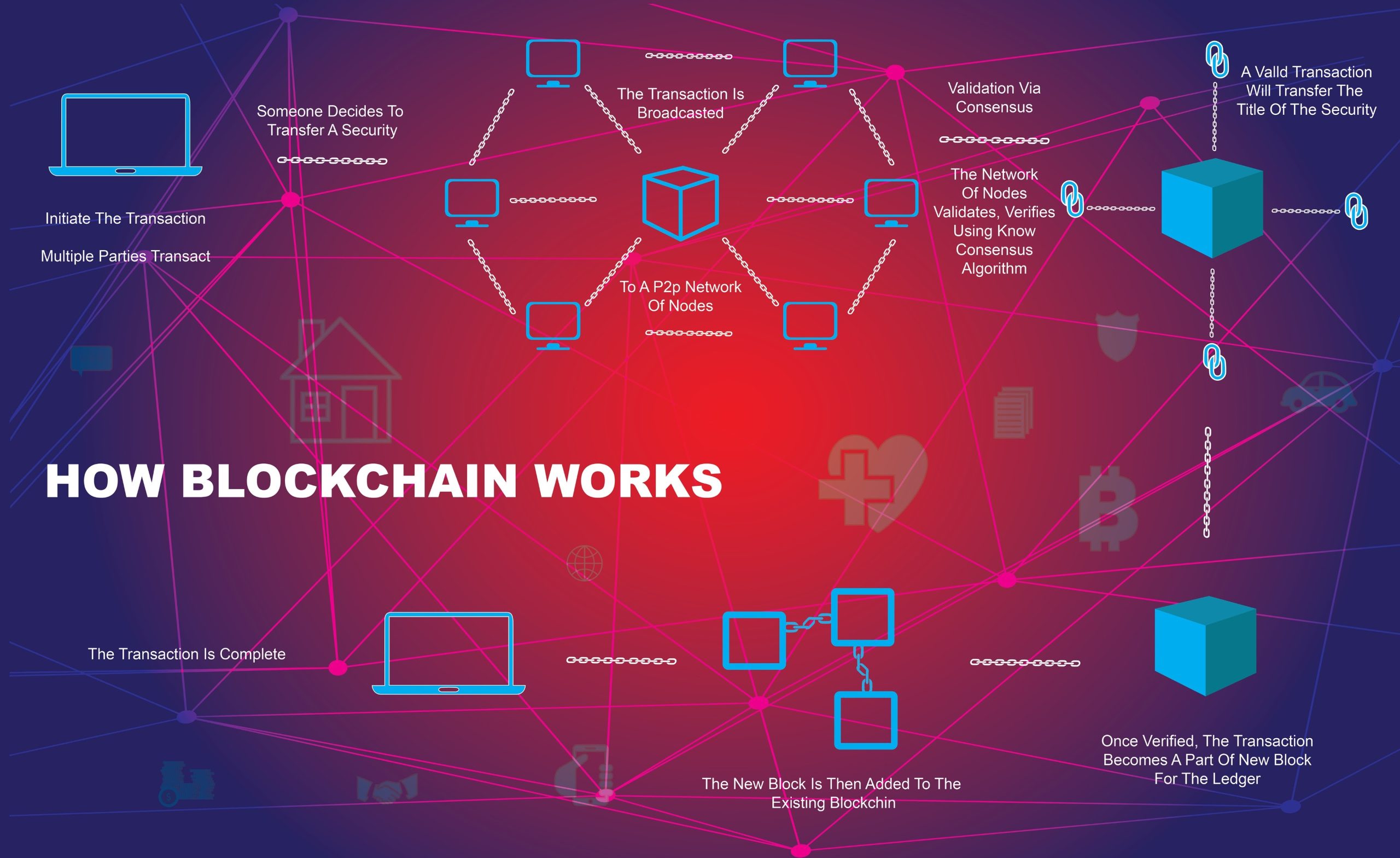

Blockchain finds major use in banking and agriculture

Many African nations face challenges like limited digital infrastructure and low trust in traditional systems, but blockchain is starting to change that.

It offers a secure, verifiable way to create and manage digital identities — a key step toward financial inclusion and better access to government services for millions of unbanked citizens.

In agriculture, blockchain supports ESG-compliant traceability, allowing consumers to follow the journey of their food from farm to table. This kind of transparency not only meets global standards but also strengthens the position of local farmers.

It is being used to secure land ownership records, provide micro-financing to smallholder farmers, and ensure fair insurance payouts.

This directly tackles issues of fraud and inefficiency that have long affected the sector, which is the backbone of many African economies.

Examples are Ripple’s RLUSD-based drought insurance pilot in Kenya, conducted in collaboration with Mercy Corps Ventures and DIVA Donate.

The program insured over 500 pastoralists, 70 percent of them women, using satellite-derived NDVI data to automatically trigger payouts of $75 in stablecoin to participants when vegetation levels dropped below a critical threshold.

Likewise, blockchain is also reshaping cross-border payments and remittance services in the banking and financial services sector by offering faster, cheaper, and more transparent alternatives to traditional banking systems.

This is essential in Africa, where remittance fees remain among the highest globally — sometimes exceeding 8 percent per transaction.

In regions with a large diaspora, such as Nigeria, Kenya, and Ghana, millions rely on funds sent home for daily living, education, and healthcare.

Blockchain-powered platforms like Yellow Card, Afriex and Chipper Cash are reducing costs and settlement times, making it easier for families to receive support without losing their money to high fees or excessive delays.

The regulatory balancing act

Now, these practical applications are gaining confidence, which is translating into a significant influx of venture capital.

The report reveals that blockchain startups attracted 7 percent of all African venture funding in 2024, totalling $122.5 million.

This is not just about the money; it’s about the quality of the investment. Seed rounds emerged as the dominant category, indicating that investors place their bets on early-stage products with the potential for long-term, real-world impact.

This strategic investment in foundational layers paves the way for a more robust and diverse blockchain ecosystem.

But the full potential of this digital development is being held in check by a fragmented and often uncertain regulatory system across Africa.

The report notes that about 35 African nations have unclear regulations on digital assets, and several others either ban or restrict them.

This creates a high-risk environment that can deter both local and international investment.

Nigeria still stand as a global leader in adoption

Nigeria stands out as a global leader in cryptocurrency adoption, offering an example of how necessity and policy can drive innovation.

Despite earlier clampdowns, the country has shifted toward a more balanced and progressive approach to digital assets.

In late 2023, the Central Bank of Nigeria lifted the crypto transaction ban for banks, opening the way for the sector.

This move, coupled with fresh guidelines for Virtual Asset Service Providers (VASPs) by the Securities and Exchange Commission (SEC), signalled a clear intent to regulate but not to reject any crypto activity.

This decision is primarily driven by real economic needs: currency devaluation, limited access to banking, and a tech-savvy youth population eager for alternatives.

For millions of Nigerians, digital assets offer a more stable, accessible way to save, invest, and transact.

In conclusion, as Africa’s leaders and policymakers grapple with the dual challenges of risk management and fostering innovation, the path forward is clear: a multifaceted and forward-looking approach to regulation that acknowledges the potential of this transformative technology.

The traceability and transparency inherent in blockchain, for instance, could be a powerful tool for regulators themselves in the fight against illicit financial flows, an opportunity that is yet to be fully capitalised on.